HPQ

The Bank of Cisco

![]()

Cisco announced it’s intention to sell $4 billion in debt, and unlike most following the company, we don’t think it is earmarked for acquisitions.

The Offering

The $4 billion in debt is divided equally between 10-year and 30-year notes, with the 10-year yielding 4.95% and the 30-year yielding 5.95%. This is +2.2% and +2.5% over U.S. Treasury yields. This cash will be used to supplement the $2.5B in domestic cash (Oct ‘08) Cisco has on hand. Of course, Cisco also has $24.3B (Oct ‘08) in overseas subsidiaries that hasn’t been repatriated to the USA in order to avoid corporate taxes.

Cisco last issued debt almost exactly 3 years ago. The $6.5B in notes issued then were used primarily to pay for the Scientific Atlanta acquisition. Cisco got a relative bargain then by today’s standard with the bonds yielding .75% to 1% above prevailing treasury rates at the time. Cisco had $15B in liquid assets then, most of it overseas.

We acknowledge it is entirely possible Cisco is filling a war chest for acquisitions. Everyone loves to play the who-will-Cisco-buy-next-game (our longstanding bet is Adtran). Cisco CEO John Chambers answered questions in his typical guarded way during an interview last month, indicating “The perfect target is a company with 100 people and a hot product that customers are saying they should go out and buy” and “We do not believe in the acquisition of large peers in any space.”

Cisco could fund such small acquisitions out of working capital, and any large acquisitions could be funded by a bond offering after the announcement, just as they did with Scientific Atlanta. This forces one to ask the question – why did Cisco just decide to triple the amount of cash it has for domestic use if we assume it isn’t for acquisitions?

The Environment

Cash is more valuable than ever because it is now very expensive to obtain for all but the best capitalized companies. Cisco can borrow against the billions in assets sitting offshore. The problem is that many of Cisco’s customers don’t have the same hefty balance sheets. Many of them can’t get money at all.

Contrary to what you would think, corporate bond issuance is up 38% in 2009. Corporate bond yield spreads have widened in the past 12 months but have retreated from the panic highs of fall 2008. Large, well capitalized companies are tapping the market’s demand for high grade debt.

It is a different story for companies with lower debt grades. While there has been some improvement in the past months, lower grade ‘junk’ debt is anywhere between 5-7% more expensive than it was a year ago- if a company can get money at all. The number one issue facing these companies in 2009 is the availability of cash.

Cisco’s channel partners, the folks who distribute Cisco to small and medium sized accounts, can no longer borrow at LIBOR +1%. Many of the lines of credit they are using today would not be written today and if they were, written at much higher rates. In some cases lines of credit that existed one day simply vaporized the next- just ask anyone who had credit with Lehman brothers.

The Bank of Cisco

We believe Cisco is growing operating cash in order to serve as a lender of last resort to its distributors and customers. An expanded balance sheet will ensure adequate capital is available not just for its own operations, but also the operations of its channel partners and customers.

If a key distributor were to suddenly lose a line of credit because the bank underwriting it implodes, Cisco can step into the breach and act as lender. If a contract manufacturer cannot obtain inventory financing Cisco can extend terms. Just as the Federal Reserve is the lender of last resort for the nations banks, Cisco can become the lender of last resort for the supply and demand chain.

Section 6 of the Notes to Consolidated Financial Statements in Cisco’s 10Q details these financial commitments. Examination of these numbers shows that Cisco has increased its financing commitments in various areas by 50-75% over the previous year (October 08/07), a period in which total revenue grew only 5%. This is quantitative evidence that Cisco is stepping into the breach created by a collapse in the credit markets.

Competitive Advantage

There is no more powerful weapon than the cost of capital, a point often lost on the tech industry which tends to focus on datasheets and speeds and feeds. During the wars between England and France, England was able to consistently field more and better ships as a result of having a cost of capital 2% better than the French, due in part to the mercantilist nature of the English economy. Cisco, like England, is turning its lower cost of capital into a competitive weapon.

Take for instance, Hewlett Packard. Much hay has been made in the recent press about how HP is going to have a run at Cisco’s mid-range Enterprise business. But in the fiscal environment of 2009-2010 this isn’t a technology fight. It is a balance sheet fight. And Cisco can deploy billions more in working capital simply because HP is already significantly more leveraged than Cisco.

It is no secret that Huawei is aggressively taking global market share, particularly in second and third world nations. Many people mistakenly believe this is because they offer cheap prices. This is not always the case. What Huawei does consistently offer are attractive credit terms, and are often the only equipment vendor doing so. While Alcatel and Ericsson still feel the vendor financing wounds of 2001-2 Huawei has no such memory.

Case in point – Telecom Malaysia (TMNET) selected vendors for a well publicized FTTH rollout and initially selected GE-PON. Huawei, at the time, was a laggard in GE-PON technology and pushed GPON. While additional information is forthcoming from TMNET in Q109 we believe Huawei won the business with GPON not based on technical superiority but on the willingness to underwrite the financing for the deal.

Strong balance sheets are powerful weapons during times of tight credit and Cisco just loaded a fresh clip.

Fun With Market Caps

Quick, rank the 10 following companies by market capitalization from large to small. If pressed for time, try picking the three biggest and three smallest.

The End of Telecom As We Know It And I Feel Fine

Anyone know where the next ten-bagger investment is in the Telecom sector? Does anyone believe such an idea is even possible anymore?

Anyone know where the next ten-bagger investment is in the Telecom sector? Does anyone believe such an idea is even possible anymore?

Continue reading

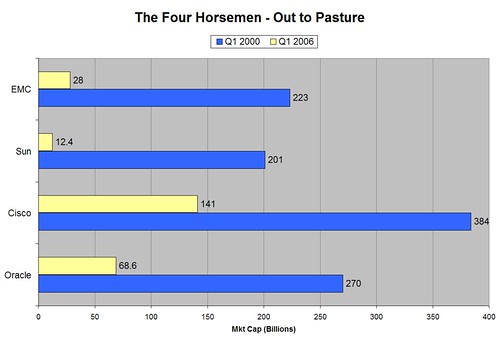

The Four Horsemen of Web 2.0

Cisco (CSCO), Oracle (ORCL), Sun (SUNW), and EMC (EMC) were the darlings of the internet boom and were referred to as the ‘Four Horsemen‘. Your broker was overheard in 2000 “Yes, things are in fact a bit irrational but these companies have real products, revenues, and earnings and are investment-grade leaders of the new economy.”

Your broker neglected to mention that the biblical Four Horsemen of the Apocalypse were steered by four riders – Conqueror, War, Famine and Death. I’ll leave it to my readers to pair them appropriately.