Article Info

The Four Horsemen of Web 2.0

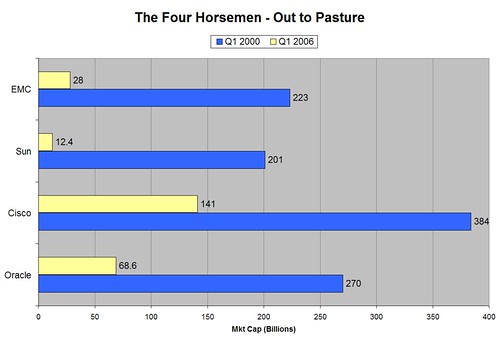

Cisco (CSCO), Oracle (ORCL), Sun (SUNW), and EMC (EMC) were the darlings of the internet boom and were referred to as the ‘Four Horsemen‘. Your broker was overheard in 2000 “Yes, things are in fact a bit irrational but these companies have real products, revenues, and earnings and are investment-grade leaders of the new economy.”

Your broker neglected to mention that the biblical Four Horsemen of the Apocalypse were steered by four riders - Conqueror, War, Famine and Death. I’ll leave it to my readers to pair them appropriately.

Today, I like to refer to Google (GOOG), Apple (AAPL), HP (HPQ), and AMD (AMD) as the new Four Horsemen of Web 2.0. Reading and listening to the media chatter about these companies induces an uncomfortable dot-com deja vu.

Bill Gates, CEO of Microsoft (MSFT) and Paul Ottellini, CEO of Intel Corp. (INTC) co-wrote an editorial in today’s WSJ. Clearly they are appealing to those who have fled their equities for the promises of Web 2.0.

Recently, we’ve read on the pages of The Wall Street Journal that we’ve reached the end of the personal computer era and that the open, broad industry approach that has enabled today’s rich computing experiences doesn’t apply to the world of digital devices.

The reality is a little different. The truth is that the model which has fueled the incredible popularity and affordability of the PC will continue to drive innovation and choice in the burgeoning area of personal devices such as cell phones, digital players and mobile PCs. As such, the PC is becoming more important and popular as a key enabler for these new digital scenarios in every corner of the world, from Indianapolis to Istanbul. If anything, it is, to paraphrase Churchill, perhaps the end of the beginning…

Gates and Otellini have a very valid point. While MP3 players, digital cameras, phones, and web based applications have stolen the show in the marketplace, all of them still rely on the PC as a digital hub. Nothing has emerged that will replace it. The only threat is the ‘thin-client’ web based application model, an idea that gets trotted out every few years and then is subsequently put back in the barn.

In addition to Intel and Microsoft, two other big-cap companies that have suffered as a result of this shift in perception are Dell Inc. (DELL) and Yahoo! Inc. (YHOO).

Competitively, all four of these companies are still forces to be reckoned with.

- Yahoo earned more money than Google in the trailing twelve months from a more diversified business model.

- Dell’s supply chain for electronics rivals Wal Mart’s in terms of efficiency and they will eventually succeed in their efforts to commoditize the consumer electronics space. The current market’s perception that PC’s are anything but commodities is a brief vacation from reality, and Dell is the best commodity producer out there. I believe the cost structure of Dell’s supply chain and web retailing model will beat HP’s.

- Intel will rip the throat out of AMD with their new low power designs for servers. They have a much bigger capital base to borrow from to build next generation fabs if (when?) money becomes more expensive. Otellini realizes the company has become too free-spending. AMD isn’t going away but the earnings multiple gap between the two is absurd.

- Microsoft has been cornered before and recovered. The Vista upgrade cycle will re-energize the cash machine. Over half of all Smartphones now run Windows Mobile 5.0 (Yes, more than Blackberry and Palm combined). Xbox 360 is looking to take share from Sony and has the best online service hands down. Meanwhile, Apple trundles along with a 5% market share in PC’s and 1/4th the valuation of Microsoft.

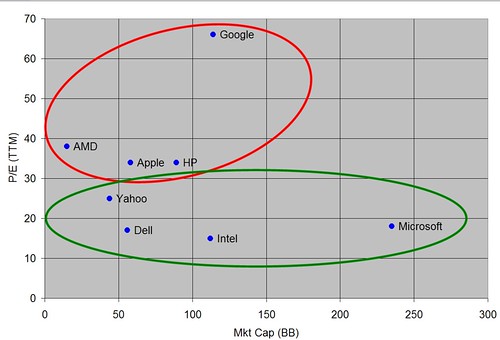

This is what the market cap vs. P/E multiple relationship looks like.

While the new ‘Four Horsemen’ may be the preferred growth engines of Web 2.0, I think these four out-of-favor companies represent a better investment vehicle for the next five years. Those with more exotic tastes can hedge by selling AMD, AAPL, HPQ, GOOG short while going long INTC, MSFT, DELL, and YHOO. This is a more market neutral strategy.

Inspiration and some data: USA TODAY

Calling a company like HP a “Web 2.0″ company makes you look like you have no clue what you are talking about. HP is a primarily a *PRINTER* company! I guess though the title will drive some traffic so even if you look a bit ignorant it won’t be all bad. Ultimately, based on your own Wikipedia reference, only the GYM players (Google, Yahoo, Microsoft) have Web 2.0 offerings.

HP has a massive presence in the Enterprise space (remember a company called Compaq and Digital) which most certainly has been impacted by the Web 2.0 phenom. All of the above companies you name, as well as the Fortune 500 buy gear from them in order to provide the back end for new web platforms.

I couldn’t agree more with the comments on Dell. Dell generates extraordinarily high returns on invested capital, has negative operating working capital (so the company actually generates cash from working capital as it grows), and has the supply chain and operation that will allow it to repeat its success in PCs in other commodity product areas. As Warren Buffett says, in a commodity business, being the low cost operator is the only defensible franchise. Dell is by far the low cost operator in the PC business, and that status will continue thanks to the advantages of its direct to consumer model.

Um HP sells overpriced printer ink, that’s about it. What about them is even remotely ‘Web’?

I think that this review is interesting but you really need to differentiate how each is contributing. I see at least four areas that each could be judged in: infrastructure, enterprise applications, business value, and user value. This might put HP in the proper location (not being compared to Google) and also promote a dialogue as to who is contributing to the Web 2.0 reality versus who is benefiting from the Web 2.0 hype.

Where’s Cisco in that 2nd chart ?

That would have been unthinkable 6 years ago . . .

Darren - I agree that the article could have been more in depth… I ended up trimming it down. The pairing is as follows

Yahoo - Google : Consumer Web Services & Media

Dell -HP : Platform Company Supplier Model

Apple - Microsoft : OS’s

Intel - AMD : Microprocessors

Barry - not a fan of Cisco because I think the Chinese are going to chip away at their margins over the next 5 years. I’ve written about SA and why I think that was a bad acquisition. COMS is more attractive with their majority exposure to Huawei-3COM.

The article cited in support for Intel outcompetting AMD seems to be just a

fanboy article that wants to sound technical, but it is not.

Intel’s current troubles have been forseen from the moment Tejas was cancelled.

That ripped apart their processor roadmap. They have managed it pretty well, but

they are still not stable yet.

Food for thought: the fact that DELL announced that for the first time they will

be using AMD processors for high end servers is not a vote of confidence on

Intel’s roadmap…

Dell changed their business model. For more than 3 years now Dell has been charging more for a pc than anyone else. They decided they were the “brand” house. “Dude, you’re getting a Dell.” After giving up the new economy definition of price leader “leading prices down,” Dell picked up the old economy definition of price leader “leading prices up.” They have improved their margins and stalled their sales growth. Dell will not recover. This party is all but over. For a very similar story see AutoZone.

Difference between Wal-mart and Dell is that

The Chinese can make and sell a PC but they can not manage a Wal-mart store in US on site….

There is a great synergy between Chinese manufacture and Walmart, and a great conflict in future between the Chinese and Dell. I think Dell will lose.

Trackbacks / Pingbacks